It’s no secret that buying a home or investment property has become harder over the last 10 years due to 2 main reason’s. Firstly, property prices have risen dramatically and secondly, banks have made changes to their requirements making it even harder to have your loan approved.

Holland Park flowering gum tree’s, Brisbane 2017.

Over the last 3 to 4 years we’ve had a steadily growing number of enquiries from people who are looking to buy a property with a family member – either one of their brothers or sisters or maybe with one or both of their parents.

I remember when I was thinking about buying my first home – at the time I had just started working and I felt that taking on the whole mortgage by myself was too much of a commitment so I decided to go in with my family: mum and dad owned a third, my brother owned a third and I owned a third.

Buying property with family provides each of you with many benefits, such as:

- it can help you buy sooner (at the time when I first bought if I had waited to do it by myself I think it would have taken me another 2 to 3 years to save the extra deposit I’d need);

- Having a lot more options as your buying capacity is higher;

- You can affording a better property in a better position (either being able to buy a house rather than a unit or being able to buy in a better suburb);

- Your financial commitments are lower (both that the deposit you need is lower and secondly that your share of the loan / repayments is a lot more manageable).

The good news is…..there are more options available now that allow people who aren’t married or in a relationship to take out a home loan together and then structure it in a way that works well for both parties.

In a typical situation, a joint home loan is designed for ‘couples or families where each person’s finances are entwined together. When I’m talking with some couples about money they generally fall into either of 2 tents.

The first boat is where you might have a couple where they’ve had a shared bank account for as long as they can remember, they often share cash that they’ve withdrawn and everything is viewed as being joint.

The second boat is where you have a situation where 2 people want to buy something together (because it makes financial sense to do this) but they’d also like to maintain their financial independence and for them buying a home or an investment property doesn’t mean having everything else all connected with that person.

This blog post is written to help people who are in the second boat!!

For example, historically, if the person you had a loan with ‘ran off’ or you had a falling out, then you were very liable for the full loan share of the loan (not just your half).

However today, lenders have moved with the times, and there have been some great improvements around how this works and the how it can benefit you as a property owner.

In this post I show you the best way to approach your home loan when buying with family.

Holland Park, Brisbane 2015.

How does the home loan work when buying property with family?

There are 2 ways a bank will set up your home loan when buying property with family:

- Buying a property together with a “joint loan” (option 2 below), or

- Buying a property together with a “property share loan” (option 3 below – I always recommend this option)

I recommend option 3, because essentially you and your brother or sister will hold separate loans.

There are several big benefits with this approach.

I’ll explain how both of these work and their pro’s and con’s through one case study based on two sisters buying in 3 different scenarios:

- Separately – option 1 (baseline case)

- As a “joint loan” – option 2 below

- As a “property share loan” – option 3 below.

Brisbane, 2015.

Case Study: Two sisters buying together

Two of my clients, sisters Lauren and Pamela, were both living with their parents when they came to see me.

They were now looking to buy their first homes, either each separately buying a unit or pooling their money and buying one bigger house in a better suburb.

Before I share with you the scenarios we went through, here is a small profile of each sister:

About Lauren

– Aged 31

-Single

-Works as a team leader in a travel agent in the Brisbane inner city

-Earns $88,000 pa (gross)

-Deposit saved of $56,000

-Has a credit card with a limit of $6,000

-Currently living with parents

-Monthly living expenses of approx. $1,200 on essentials like food, bills, board and a further $800 on discretionary spending like social life and clothes

-Major goal next 12 months: Buy unit/house to move into around Woolloongabba, Greenslopes (Brisbane Southside),

-Personal goals next 12 months: buy a set of brand new furniture that matches her home,

-Goal next 3 years: she wants to travel through Canada for at least 2 months and buy her first investment property,

-Ideally wants to meet a partner, get married and maybe start a family.

Brisbane, 2015.

About Pamela

-Aged 28

-Studied Bach Arts and completed Diploma Education

-Lived and worked in London for 2 years, before returning to Australia 3 years ago

-Works as a private school teacher on Brisbane south side

-Earns $79,000 pa (gross)

-Deposit saved of $67,000

-Has a credit card with a limit of $1,000

-Has a personal loan for a car of $14,300 repaying $289 each month

-Currently living with parents

-Monthly living expenses of approx. $900 on essentials like food, bills, board and a further $500 on discretionary spending like social life and clothes

-Major money goal: Buy unit/house to move into around Woolloongabba, Greenslopes (Brisbane Southside)

-Personal goals next 12 months: 3 week overseas holiday every year

-She’d like to meet a partner in the future (someone who loves travelling as much as she does!!)

Firstly, lets look at option 1, the scenario of both Lauren and Pamela buying their own separate places (so we can see the ‘baseline’ to compare to).

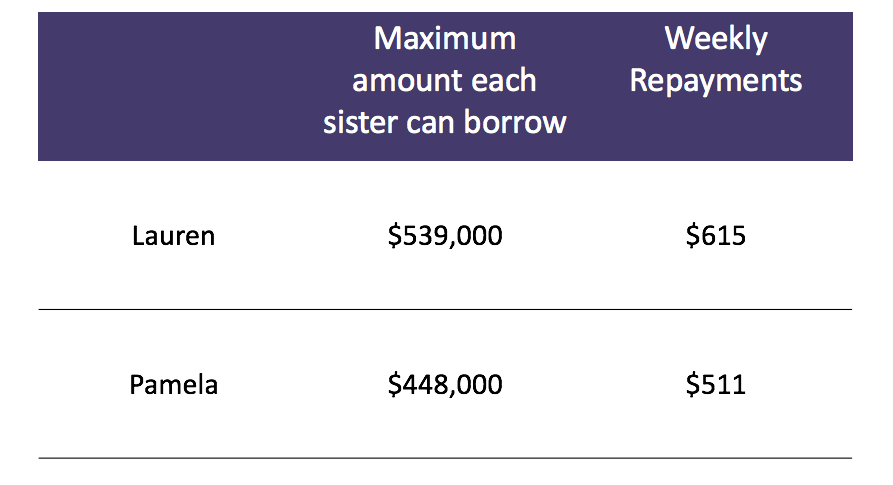

Option 1: Each sister buying their own separate properties

Based on their personal circumstances, here is how much they can borrow (see table below):

- Lauren can borrow up to $539,000 and would repay $615 each week on her loan

- Pamela can borrow up to $448,000 and would repay $511 each week

*Assumes interest rate of 4.30%, loan term 30 years

Upsides of buying separately:

- Complete freedom with each sister in her own property

- No future complications

Downsides of buying separately:

- Based on the current Brisbane market, each sister can only afford a 2 bedroom unit or a small older house, as they can only borrow $539,000 and $448,000 respectively.

Greenslopes Parklands, Brisbane 2015.

Now I’ll walk through the two different options the sisters have if they choose to buy a property together.

Option 2 is a ‘joint home loan’ and option 2 is a ‘property share loan’.

I always recommend option 3, the ‘property share loan’ to my clients.

Option 2: Getting a ‘joint home loan’

This has traditionally been the most common approach to buying property with someone, either a partner or a family member.

In this situation, there is one home loan that both siblings are applicants for. The loan is based upon the combined financial strength of both parties.

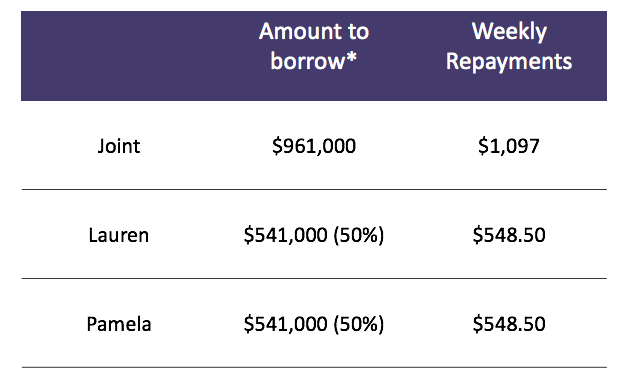

The results when buying as a joint loan (table below)

- Bigger joint borrowing capacity, borrowing up to $961,000

- Add on the combined deposit saved of $122,000, so the maximum amount they have to spend on a home and buying costs is $1,083,000 (ie 961,000 + $122,000)

- Buying costs (stamp duty, solicitors fees, transfer fees etc) of $22,000

What to do when siblings have different deposits to contribute

Lauren has saved $56,000 as a deposit, which is less than her sister Pamela at $67,000, however they both want to own the property 50/50.

This means Lauren will need to borrow slightly more than her sister (see table below).

Lauren borrows $485,000 and Pamela borrows $474,000 (if they had equal deposits they would borrow $541,000 each).

Lauren’s loan repayments will be higher at $554 a week and Pamela’s are $541.

*Assumes interest rate of 4.30%, loan term 30 years

Avoid the temptation to borrow the maximum amount you are approved for

In this situation, I would not recommend for Lauren and Pamela to borrow the full $961,000.

This is because the purpose of buying together was to make the loan repayments more manageable and at the same time buy a better home.

If they borrowed the full $961,000, I feel this loan to big for them to manage, especially if interest rates rise or there are unexpected costs in their lives (which is likely).

It’s better to borrow an amount you feel comfortable repaying

Instead, Lauren and Pamela decided on a house in Greenslopes for $710,000.

After adding on costs of buying, the total amount needed is $732,000.

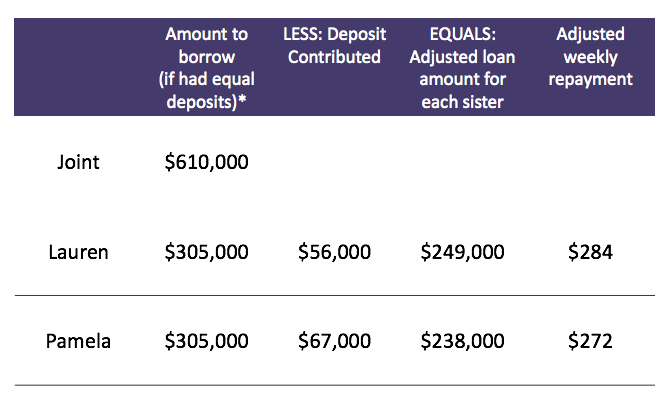

Using their full deposit of $122,000, this means they now need to borrow $610,000.

Cost of house: $710,000

Costs of buying: $22,000

Total amount needed: $732,000

LESS: Deposit $122,000

Total loan required $610,000

Since Lauren is putting in less of a deposit compared to Pamela, she now needs to borrow slightly more money.

With the adjusted loan amounts, Lauren ends up borrowing $249,000 and repaying $284 each week (see table below).

Pamela borrows $238,000 and repays $272 each week.

Compared the baseline scenario I covered above (where the sisters buy property separately). this option with a joint loan is far more manageable financially.

*Assumes interest rate of 4.30%, loan term 30 years

Greenslopes, Brisbane 2015.

Upsides of a joint loan compared to buying separately

- Combined buying power means a better house in a better suburb (if they were to borrow the full amount)

- Lower weekly repayments

- Allows them to own a share in a house in a better position rather than a unit

Downsides of a joint loan compared to buying separately

What I explain here, is one of the most important facts to understand about getting this type of joint loan.

Make sure you read option 2 below on property share loans, as you can avoid some of these issues.

Downsides of a joint loan:

1. The bank will hold each sibling liable for the full loan of $610,000 – this is the major downside of a joint loan.

It impacts you if, say if one of you loses your job, you have a fall so runs away and can’t pay your share of the loan, then the other partner will be fully liable for both shares of repayments.

2. If one sibling wants to buy another home, for example, if your settling down with a partner, then your borrowing capacity is greatly reduced.

Nearly all banks and financial institutions will calculate your borrowing capacity as already having a $610,000 loan.

This is very likely to mean that you won’t be borrowing much money in the future as you will be reaching your ‘borrowing capacity’ (the maximum amount you can borrow).

This could be an issue, if for example, you wanted to buy with your wife/partner (and keep this house with your family).

Brisbane Eye, Southbank, 2015.

Option 3: ‘Property share loan’ (recommended)

The second type of loan is one that’s only offered by the Commonwealth Bank (CBA) and it’s currently a unique type of loan facility for the situation for Lauren and Pamela.

Note, I am in no way associated or incentivised by CBA for this post. This recommendation is based on my experience as a mortgage broker working with over 40 different lenders and thousands of different loan types.

I am really comfortable recommending this option to you as I’ve seen it successfully work with other clients.

A property share loan is different from the traditional joint loan as shown in option 1 as:

- Each applicant has their own separate home loan

- Both loans are secured against the same property.

The numbers when buying as a property share loan

Using the same situation as in Option 1, where they purchased a house in Greenslopes for $710,000, the numbers are the same.

House price: $710,000

Costs to buy: $22,000

Total (house + costs of buying) : $732,000

*Assumes interest rate of 4.30%, loan term 30 years

Upsides of property share loans

Major benefits as to why I recommend this type of loan:

- You each have a smaller loan – this is the MAJOR benefit when you go to buy another property in the future, say with a new partner, because your borrowing capacity isn’t significantly reduced. The bank will only account for your half of the loan so Lauren will be assessed as having already borrowed $249,000 (compared with the $610,000 she would have against her name if she went with option 1).

- Each person can pay out their loan in their own time – so if you want to make extra repayment but your sister doesn’t, you take all the benefit of paying your share off sooner.

Downsides of property share loans

- Currently the only bank offering Property Share loans is the Commonwealth Bank (which should only be an issue if you don’t like them)!

- Each person has to apply individually for their own home loan – this means both loans have to be approved in order for the home purchase to be approved at the same time.

So if one of you has a bad credit history from not paying bills or credit cards on time, for example, then it will effect both of you as they may not be able to get a loan.

Wrap up

Buy now I hope it’s obvious the benefits of buying property with your siblings!

The key points to know are that it propels you into the property market sooner, and with the Property Share Loan, you can be sure you’re each protected.

The information contained within this page is general in nature. It serves as a guide only and does not take into account your personal financial needs. Before you act on this information you should seek independent legal and financial advice. Copyright Blackk Finance 2017.